Thailand’s Stalled Transition to Electric Motorcyclces

Tom Courtright · 17 November 2025

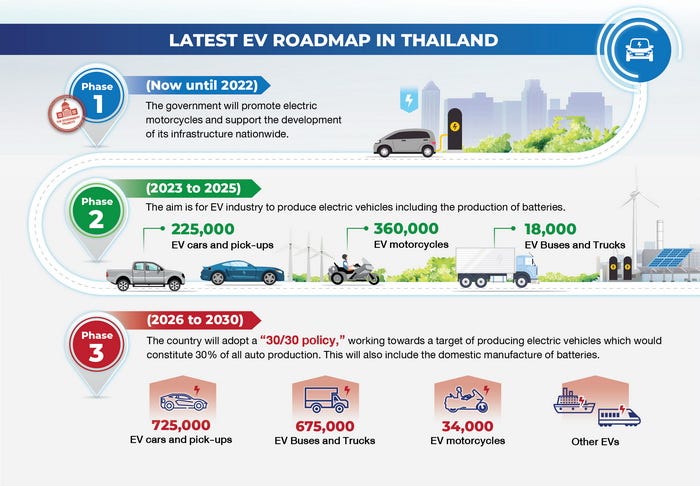

Bangkok’s streets are increasingly filled with sleek Chinese electric cars — BYD sedans drive past malls and food stalls, and Neta EVs queue at charging stations. The government has set up an ambitious “30@30” policy to become a regional electric vehicle production hub. By 2030, 30% of all vehicles (both on the road and produced) should be electric, with a short-term goal of 20% by 2025.

Yet while the four-wheel segment races ahead, the electric two-wheeler sector has stalled. In 2024, electric motorcycle sales collapsed by over 50%, and their market penetration was only 1.3% of sales in 2025. Compare this to Uganda, which has around 5–10% sales share this year, or the smaller market Kenya which has over 10%.

This isn’t for lack of favorable conditions. Thailand doesn’t subsidize fuel prices the way Nigeria or Egypt does — a liter of fuel goes for 31 THB ($1.00, or 3,500 UGX). The country boasts one of Southeast Asia’s most reliable and extensive electricity grids. Doing business here is relatively straightforward — Thailand economically benefitted from being a US and Japanese ally during the cold war and consistently ranks among the region’s easiest places for foreign direct investment. The government has poured incentives into the sector through the BEV 3.0 and BEV 3.5 policies, offering tax breaks and subsidies for electric vehicle adoption, including up to 530 USD subsidies for e-motorcycles.

So why are electric motorcycles slowing down while electric cars accelerate?

A Commuter-First Market

The first barrier is structural. Thailand’s motorcycle market is dominated by personal ownership, not commercial use. Unlike in Kampala, where boda bodas likely make up over 80% of motorcycles, most Thai riders use motorcycles for personal trips, doing perhaps 40 km / day.

The primary reason for transitioning to e-motorcycles (apart from forceful government policy) is usually to save on fuel costs, which of course increase significantly the more you drive. Boda riders in East Africa driving anywhere from 80–200 kilometers per day see significant benefits in reducing the money they lose to Shell and Rubis stations. For a Bangkok resident using their bike for a 20-kilometer commute and weekend errands, that payback period stretches uncomfortably long.

Thailand has an estimated 100,000 motorcycle taxi drivers — the orange-vested win drivers standing at stages throughout Bangkok (and an unknown number more on Grab). But they represent a tiny fraction of the country’s 20+ million registered motorcycles. For personal users, the math isn’t mathing, especially when a conventional Honda Wave 125cc costs around 54,000 baht ($1,800) while electric alternatives start considerably higher — because you need to buy the battery, as we’ll explain briefly. Additionally, personal motorcycles last much longer — around 10 to 20 years in Thailand— and thus the opportunities to buy a new one (and transition to electric) are fewer.

The Battery Ownership Roadblock

The second barrier is bureaucratic but devastating: Thailand’s Department of Land Transport (DLT) requires that any motorcycle registered — whether for commercial or personal use — must include the battery as part of the registered vehicle. You cannot register a motorcycle without owning its battery.

This single regulation has strangled the battery-swapping business model that has proven successful elsewhere in Asia and East Africa.

Without the ability to register a vehicle separately from its battery, battery-as-a-service models become legally impossible. The few battery swap systems operating in Thailand — like Winnonie, which serves over 1,000 riders, or PTT’s now-discontinued Swap & Go — have to conduct rental-only arrangements, which are not particularly attractive. The company owns both the motorcycle and the battery, renting the complete package to riders. Drivers never own the vehicle, remaining perpetually dependent on a single provider. Grab, the dominant ride-hailing app in Thailand, provides a rental system that costs riders around $5 a day.

These rental systems have unfortunately gone the way of Gogoro and don’t charge based on state-of-charge or energy consumed, instead setting a flat rate for a maximum number of swaps per month, creating perverse incentives that have nothing to do with actual energy usage. A rider who does short trips with frequent swaps subsidizes another who drains each battery completely. The economics haven’t worked for Gogoro, and they fundamentally don’t feel fair to riders.

Industry representatives report raising this issue with the DLT for years, to no effect. Meanwhile, the motosae (boda boda) segment — the one group that could make electric economics work — remains locked out of battery swapping.

Honda’s Stranglehold

The third factor is Honda’s market dominance and strategic inaction. Honda controls roughly 77–80% of Thailand’s motorcycle market. Their assembly plants dot the Eastern Economic Corridor. Their dealer network reaches every town. Their financing arms make purchasing a conventional bike effortless for Thai consumers (and at highly enviable rates of around 10% a year, compared to the 40–60% paid in East African markets).

Honda is a founding member of the Swappable Batteries Motorcycle Consortium (SBMC), announced with much fanfare in 2021 alongside Yamaha, KTM, and Piaggio. The consortium promised standardized swappable batteries for electric two-wheelers across the industry. When I met a representative two years ago in Germany and asked if they would develop a 72V battery for Africa, he shrugged, and told me Africa would follow Asia. Since then, Africa has sped ahead, while the SBMC limps on.

This shouldn’t surprise anyone familiar with how legacy automakers view electrification. Honda, like Toyota and other Japanese manufacturers, has been conspicuously slow on EV adoption globally. In Japan itself, the automotive industry continues pushing hydrogen fuel cells as an alternative, a technology that conveniently preserves the oil and gas industry’s role in the transportation system. The entrenched relationship between Japanese automakers and the petroleum sector — along with concerns about cannibalizing their existing, highly profitable conventional motorcycle business — creates every incentive to slow-walk electric adoption.

Why invest billions retooling Thai factories for electric motorcycle production when conventional bikes still sell well and carry higher profit margins? Why risk disrupting dealer networks built around engine maintenance and spare parts sales? Why rush to undermine your own dominant market position?

The economic logic for Honda is clear: delay as long as possible while maintaining the appearance of participation in the electric transition.

Selling Dreams, Not Motorcycles

Before you even get to the regulatory barriers and incumbent resistance, however, Thailand’s shopfronts will tell you something else: many of the electric motorcycles available are simply not very good products, and they are far from the affordability and quality nexus.

First, there is still significant overpromising in terms of range. Models regularly promise over 100 km range on batteries with less than 2 kWh capacity. This would mean over 50 km range per kWh — over double the real-world average in East Africa. E2W retailers interviewed for this article described slowing sales as customers came back complaining about battery capacity.

There’s also almost no aftermarket support. When a conventional Honda breaks down, repair shops exist on virtually every corner. Parts are everywhere, and any mechanic can fix it. For e-motorcycles, however, parts regularly have to be ordered from the OEM, as retailers aren’t keeping enough in stock.

This also reflects a fundamental difference in business models between Thailand and East Africa. Hapa Afrika Mashariki, the e-boda companies Gogo, Ampersand, Zembo and the rest are in the business of providing battery swapping services. This means they’re invested in long-term customer satisfaction because their revenue depends on drivers continuing to use their swap networks. If the motorcycles break down or batteries are falling far short of claimed range, riders protest, switch motorcycle, and the company loses its revenue stream. This has helped companies in East Africa rapidly iterate on motorcycle design and learn from field failures.

In Thailand, by contrast, manufacturers can sell motorcycles and walk away. The result is a market flooded with underdeveloped products making unrealistic claims, sold to buyers who discover too late that support doesn’t exist. This compounds the other barriers — even riders willing to take a chance on electric find themselves stranded with expensive paperweights when something inevitably goes wrong.

The DLT’s battery registration requirement ensures that the battery-as-a-service model that drove quality improvements in Africa can’t emerge in Thailand. And without that function, manufacturers face no market pressure to build better products or provide real support. They can keep selling dreams instead of motorcycles, knowing the next buyer hasn’t heard about the problems yet.

What Happens Next?

Thailand’s 30@30 target for motorcycle production — 675,000 electric units annually by 2030 — is not going to be reached at this rate.

Unless the DLT changes its battery registration requirements, new entrants have no realistic path to disrupt Honda’s comfortable position. Gogoro won’t come (and has bigger issues to solve anyway, like becoming profitable). Local startups can’t scale. Battery swapping remains stuck in limited rental-only pilots that will never achieve the network effects needed for mass adoption.

The commercial motorcycle taxi segment — the one group that could drive electric adoption through pure economics — remains locked out of the technology that would work best for them. The win drivers continue buying conventional Hondas on installment plans, racking up kilometers on gasoline engines, because the alternative simply doesn’t exist in a viable form.

Bangkok’s streets may soon be full of Chinese electric cars, but the highly-regulated orange-vested motosae riders weaving between them will likely still be riding petrol Hondas for years to come. All because a combination of regulatory barriers and incumbent resistance has made sure the electric option never actually arrives.